“The Strait Is Disrupted. The Green Fuel Is Concentrated. And Your Ship Still Needs to Move.”

You’re scrolling your feed. Headlines about green methanol milestones. Ammonia bunkering standards. Oil price volatility. The conversation around alternative fuels in shipping was about saving the planet three months ago. Today, it’s about keeping the lights on

Three months ago, the conversation was about saving the planet.

Today, it’s about keeping the lights on.

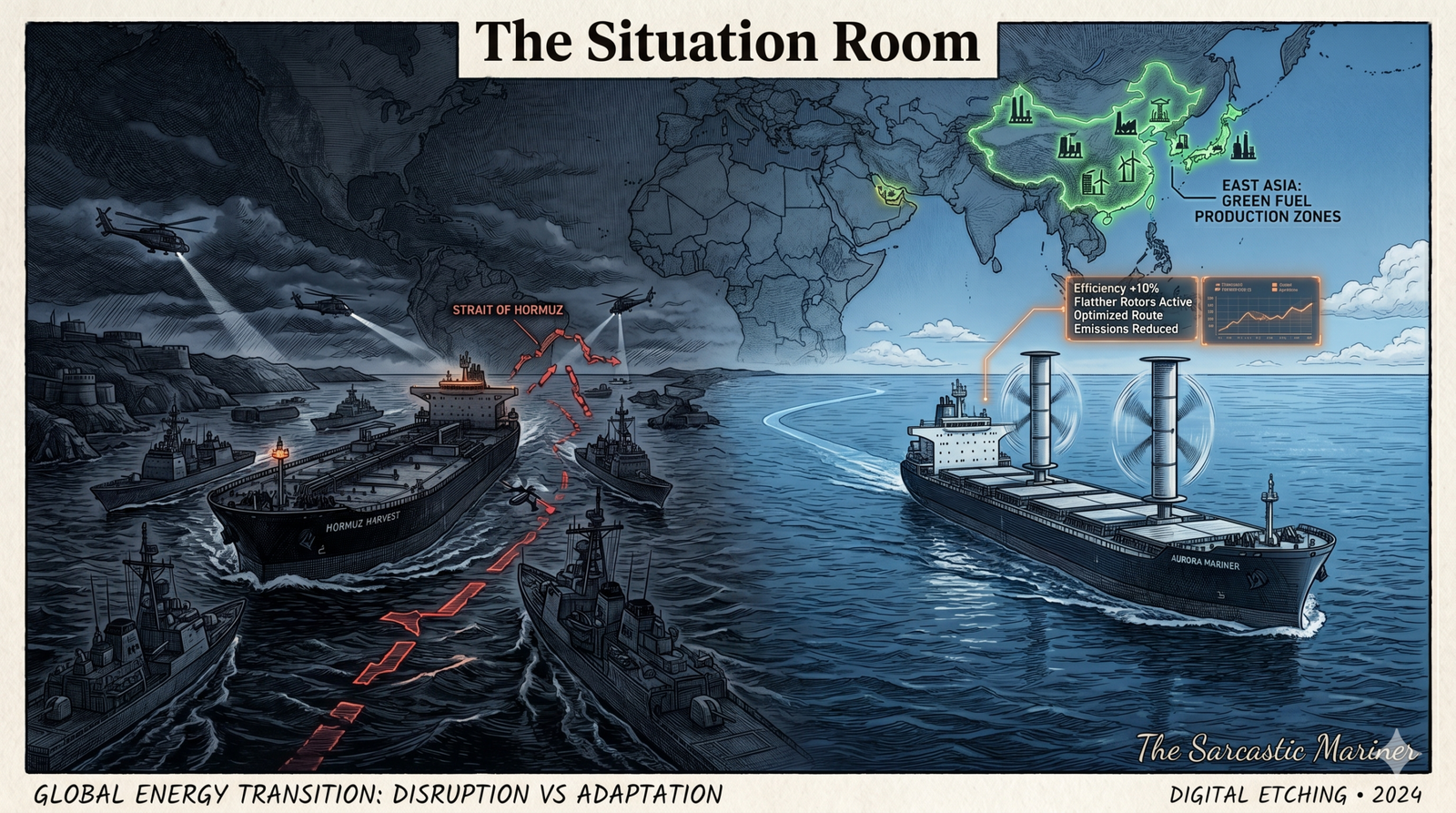

The disruption in the Strait of Hormuz has done what no environmental regulation could: it forced energy security back to the top of the agenda.

Green fuels? Still coming. Still unevenly distributed.

But when your bunkers sit across a high-risk corridor, sustainability quickly becomes… a logistics problem.

We went digging. Here’s what the situation looks like as at end May 2026.

Q1: The Strait of Hormuz is disrupted. How is that affecting fuel prices—and the push for alternatives?

The Non-Expert Says: Oil is volatile. Alternatives are still expensive. And uncertainty is driving decisions.

The Strait of Hormuz—handling roughly 20% of global oil trade—has not fully “closed,” but remains highly disrupted, with periodic transit slowdowns, rerouting, and elevated war risk premiums.

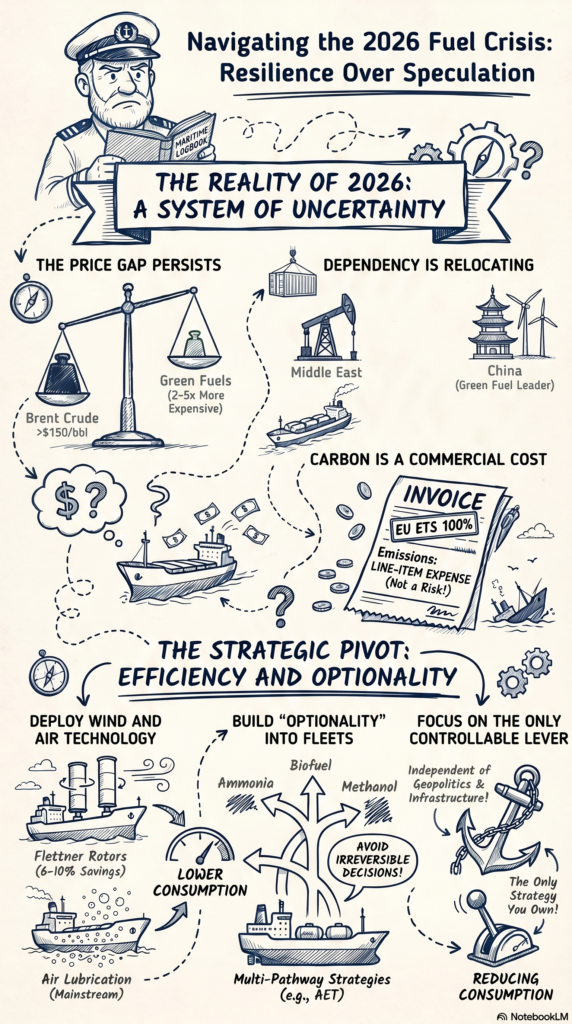

Oil markets reacted accordingly. Brent crude spiked toward the $115–120 range in March before stabilising, with upside scenarios (including Citi forecasts) still pointing toward $130–150 if disruptions escalate.

Alternative fuels, meanwhile, remain structurally more expensive. Industry data—including DNV assessments—continues to place many low-carbon fuels at 2–5x the cost of conventional marine fuels, depending on scale and production pathway.

The TSM Take:

When oil is cheap, we talk transition.

When oil spikes, we talk resilience.

The transition hasn’t stopped—it’s just being repriced in real time.

Q2: Who actually controls the production of green methanol and ammonia?

The Non-Expert Says: Production is scaling—but unevenly, with China currently leading capacity build-out.

China has rapidly expanded its position in green fuel production, with significant capacity across green ammonia, methanol, and synthetic fuels. Planned and operational capacity runs into millions of tonnes annually, with particularly strong momentum in green methanol.

Europe and the U.S. continue to invest, but commercial-scale deployment remains slower and more fragmented.

The TSM Take:

We may be reducing dependence on oil. The alternative fuels in shipping landscape is diversifying — but concentration of supply is simply shifting geography, not eliminating it.

Different fuel. Different geography. Same strategic question: Who controls supply when it matters?

This is the same strategic logic playing out in insurance — as we explored when India made its sovereign play against the P&I system. Different lever. Same question: who controls the chokepoint?”

Q3: What about fuel-saving tech like Flettner rotors and air lubrication? Are those viable alternatives?

The Non-Expert Says: Yes—and they’re being deployed now, without waiting for fuel certainty.

Wind-assisted propulsion is gaining traction. Large-scale operational data (over 1.7 billion km of voyages) suggests 6–10% average fuel savings, with higher gains on suitable vessel types.

The technology is scaling:

- Rotor sails being deployed via partnerships (e.g., COSCO & Anemoi)

- Systems already operational across multiple fleets

- Large vessels (including Valemax class) now integrating wind assistance

Air lubrication is also moving from niche to mainstream:

- Over 150 vessels in operation

- 250+ systems on order

- Expanding OEM adoption across newbuilds and retrofits

The TSM Take:

While the industry debates future fuels,

someone quietly reduced consumption—today.

Not headline-grabbing.

But very bankable.

Q4: If these technologies work, why isn’t everyone installing them?

The Non-Expert Says: Because uncertainty still dominates investment decisions.

Alternative-fuel vessel orders slowed in early 2026, reflecting hesitation across the market. Owners are balancing:

- Fuel uncertainty

- Infrastructure gaps

- Regulatory timing (IMO Net-Zero Framework still pending)

- Asset lifespan considerations

This isn’t resistance—it’s risk management.

The same leadership blindspot shows up across shipping — we’ve written about how maritime safety culture rewards the appearance of decisions over the quality of them.

The TSM Take:

Shipowners aren’t avoiding change.

They’re avoiding irreversible decisions in an uncertain system.

In shipping, doing nothing is often a strategy—until clarity arrives.

Q5: Is there a “green fuel of the future” emerging as a clear winner?

The Non-Expert Says: No single winner—yet.

The alternative fuels in shipping market isn’t a race with one finish line. It’s a portfolio decision — with incomplete data

Each option presents trade-offs:

- Methanol: scalable, but carbon intensity varies by source

- Ammonia: zero carbon at use, but toxic and infrastructure-light

- Hydrogen: clean, but complex storage and economics

- Biofuels: near-term viable, but supply-limited

The TSM Take:

This isn’t a race with one finish line.

It’s a portfolio decision—with incomplete data.

And no industry-wide agreement on the strategy.

Q6: The EU ETS is now fully in force. How does that change the equation?

The Non-Expert Says: It makes carbon a cost—today, not tomorrow.

As of January 2026, shipping is fully integrated into the EU ETS, requiring operators to cover 100% of emissions exposure within scope.

This introduces immediate financial impact:

- Carbon becomes a line item, not a future risk

- Compliance decisions become commercial decisions

- Biofuel blending and credit strategies gain traction

The TSM Take:

The EU didn’t wait for consensus.

They priced carbon—and let the market respond.

And when cost shows up, behaviour follows.

Q7: So what should shipowners actually do—wait or invest?

The Non-Expert Says: Invest selectively. Stay flexible. Avoid overcommitment.

The emerging approach is multi-pathway:

- Efficiency upgrades

- Fuel flexibility

- Regulatory alignment

- Incremental exposure management

Operators like AET are pursuing diversified fuel strategies—not betting on a single outcome.

Meanwhile, efficiency technologies remain the lowest-risk investments:

- Fuel-agnostic

- Proven returns

- Independent of geopolitical disruption

The TSM Take:

Don’t pick a winner.

Build optionality.

And reduce consumption—because that’s the only lever fully under your control.

Why the Alternative Fuels IN Shipping Transition Is Happening Unevenly

TSM Situation Room Takeaway

The Hormuz disruption exposed a hard truth:

Alternative fuels in shipping are not a shortcut to energy security.

They introduce a different set of dependencies.

But the situation also accelerated something important:

a shift toward solutions that don’t rely on external certainty.

- Efficiency over speculation

- Flexibility over commitment

- Adaptation over prediction

The green fuel transition is real.

But it is not evenly distributed—and not yet fully operational.

In the meantime:

Ships still need to move.

Cargo still needs to deliver.

And decisions still need to be made under uncertainty.

The near-term winners won’t be those who guessed the right fuel.

They’ll be the ones who:

- Reduced consumption

- Maintained flexibility

- Avoided locking in too early

The TSM Final Word

The Strait is disrupted.

The green fuel is concentrated.

And your ship still needs to move.

The alternative fuels in shipping debate will continue. So install what works. Reduce what you can. And don’t wait for a global consensus—

Because the only thing the industry agrees on… is that it doesn’t agree.

The Sarcastic Mariner(s)…

Stirring the pot so the industry remembers how to think.

The industry has opinions on this. Some of them are even correct. We took this conversation to LinkedIn — come tell us where we’re wrong. 👉 Join the discussion on LinkedIn

Disclaimer

Disclaimer: The Sarcastic Mariner(s) are not futurists, energy analysts, or policy wonks. We’re just people who read a lot of maritime news so you don’t have to. The following is based on actual events, real data, and a healthy dose of skepticism. Facts are cited. Opinions are ours. Use at your own risk.